A short presentation I gave last night to a business audience at Creative Lancashire.

Here is a list of relevant links I provided for the audience.

Thursday, 20 November 2008

Wednesday, 12 November 2008

How "recession-proof" is your business?

The most popular boast now from entrepreneurs seeking funding is that their business is, to some degree, "recession proof". Whilst it will be some time before we know the magnitude and implications of the economic situation, we can attempt to help our portfolio companies understand how vulnerable they may be.

Fred Wilson had an excellent post on the strength of his portfolio using something he dubbed The Survival Matrix. I thought I'd extend this a little by putting together a kind of recession-proofness-test that draws in some of the other issues. Please take the precise numbers with a big "pinch of salt": I am not planning on defending any of the weightings or rankings. I'd welcome any debate about what's included, but my purpose is to highlight issues and help give people a feel for where they stand.

When I tried this test on a few portfolio companies it certainly showed a wide disparity. At the lowest 45 points and the highest 109 points out of a theoretical maximum of around 220. My view is that companies upto perhaps 50/60 points really need to think hard and urgently about making what might be quite big departures from plan. Whereas around "100 points" perhaps a slightly more considered view makes more sense even if the actions taken are still pretty firm. I can't imagine many VC-backed companies will get anywhere close to 200!

I hope this test helps a little for companies to focus on just how much and how urgently their plans need to adapt. I'm doing a presentation around this stuff at our portfolio seminar this morning which I'll post up too.

You can find the calculator here.

The most popular boast now from entrepreneurs seeking funding is that their business is, to some degree, "recession proof". Whilst it will be some time before we know the magnitude and implications of the economic situation, we can attempt to help our portfolio companies understand how vulnerable they may be.

Fred Wilson had an excellent post on the strength of his portfolio using something he dubbed The Survival Matrix. I thought I'd extend this a little by putting together a kind of recession-proofness-test that draws in some of the other issues. Please take the precise numbers with a big "pinch of salt": I am not planning on defending any of the weightings or rankings. I'd welcome any debate about what's included, but my purpose is to highlight issues and help give people a feel for where they stand.

When I tried this test on a few portfolio companies it certainly showed a wide disparity. At the lowest 45 points and the highest 109 points out of a theoretical maximum of around 220. My view is that companies upto perhaps 50/60 points really need to think hard and urgently about making what might be quite big departures from plan. Whereas around "100 points" perhaps a slightly more considered view makes more sense even if the actions taken are still pretty firm. I can't imagine many VC-backed companies will get anywhere close to 200!

I hope this test helps a little for companies to focus on just how much and how urgently their plans need to adapt. I'm doing a presentation around this stuff at our portfolio seminar this morning which I'll post up too.

You can find the calculator here.

RisingStars Portfolio Seminar- A constructive look at technology companies in the recession

Jonathan Diggines our CEO opened the event with a view of the state of the economy generally: hard to make this part positive looking, but Jonathan pointed out that there's no reason to think that tech sector will be worse effected, and some reason to think it might be better than most.

Jonathan Diggines our CEO opened the event with a view of the state of the economy generally: hard to make this part positive looking, but Jonathan pointed out that there's no reason to think that tech sector will be worse effected, and some reason to think it might be better than most.

Julian Viggars looked then at our portfolio in more detail, and about technology generally. It was great to hear a summary of some of the great progress in terms of further fundraising and commercial progress drawn together. He produced some interesting comments from some of the top-tier tech companies: Cisco, SAP, Google. The key thing was a big disparity between how different sectors saw the outlook.

Julian Viggars looked then at our portfolio in more detail, and about technology generally. It was great to hear a summary of some of the great progress in terms of further fundraising and commercial progress drawn together. He produced some interesting comments from some of the top-tier tech companies: Cisco, SAP, Google. The key thing was a big disparity between how different sectors saw the outlook.

Stuart McKnight, the Managing Director of Ascendant Corporate Finance, after the obligatory quick plug, provided lots of current data on the state of the tech financing market. With 282 live technology investors who did deals in 2007 over £0.5m last year. With 2/3rds of deals being 2nd round or later, then that left only 78 first rounds above £0.5m. By the end of Q3 2008 it looked like the rate of capital investment was slightly faster than 2007, with very little sign of any negative change in the first 3 quarters of the year at least. Stuart's view is that the Limited Partnership structure means that is still plenty of reason for funds to keep on investing. Reckons the market will be at around £900m in 2009- up a bit from the current rate, with a continued rise in "cleantech" as a sector through that period with several new funds having closed. He said lovely things about Acal and their team, which is nice, but observed that the fundraising had been more challenging that anticipated because so many of these new funds are late stage and there's a gap beneath this level.

Stuart was concerned that there was a shift away from small scale investing, with a drop in the proportion of deals in the £200k-£1m range. He thinks that companies are finding seed funding, but hitting a gap at the first proper VC round. He speculated that maybe the recession will push some of the VC's to decrease deal size, pushing down total value faster than volume.

Looking at regional patterns, I was surprised that the Thames valley, including Oxford, was a really small area, less than half that of the Northern region. So far London is the only region where volume and value have started to show a downturn. Stuart thinks that 2009 will be strongly indicated by the impact on Q4 2008. He knows of four funds that have said they have no intention of investing in the quarter, claiming that they want to hang on to cash to support portfolio.

Stuart summed up with a great set of conclusions- more and better of the usual good stuff likely to be required by companies seeking finance. He sees that the best stuff will still raise money, but that you need to expect everything to be a bit slower and tighter in the next 12 months. You need to expect to double the work on fundraising- maybe 40-50 VC's approached, 20 or so first meetings, and spreading your net wider than might once have been required.

Stuart McKnight, the Managing Director of Ascendant Corporate Finance, after the obligatory quick plug, provided lots of current data on the state of the tech financing market. With 282 live technology investors who did deals in 2007 over £0.5m last year. With 2/3rds of deals being 2nd round or later, then that left only 78 first rounds above £0.5m. By the end of Q3 2008 it looked like the rate of capital investment was slightly faster than 2007, with very little sign of any negative change in the first 3 quarters of the year at least. Stuart's view is that the Limited Partnership structure means that is still plenty of reason for funds to keep on investing. Reckons the market will be at around £900m in 2009- up a bit from the current rate, with a continued rise in "cleantech" as a sector through that period with several new funds having closed. He said lovely things about Acal and their team, which is nice, but observed that the fundraising had been more challenging that anticipated because so many of these new funds are late stage and there's a gap beneath this level.

Stuart was concerned that there was a shift away from small scale investing, with a drop in the proportion of deals in the £200k-£1m range. He thinks that companies are finding seed funding, but hitting a gap at the first proper VC round. He speculated that maybe the recession will push some of the VC's to decrease deal size, pushing down total value faster than volume.

Looking at regional patterns, I was surprised that the Thames valley, including Oxford, was a really small area, less than half that of the Northern region. So far London is the only region where volume and value have started to show a downturn. Stuart thinks that 2009 will be strongly indicated by the impact on Q4 2008. He knows of four funds that have said they have no intention of investing in the quarter, claiming that they want to hang on to cash to support portfolio.

Stuart summed up with a great set of conclusions- more and better of the usual good stuff likely to be required by companies seeking finance. He sees that the best stuff will still raise money, but that you need to expect everything to be a bit slower and tighter in the next 12 months. You need to expect to double the work on fundraising- maybe 40-50 VC's approached, 20 or so first meetings, and spreading your net wider than might once have been required.

Richard Young told the seminar about his experiences of the last recession, and reflected on how one of our companies, Blue Prism, is adapting to the new reality in Enterprise Software by adapting their customer messaging and propositions.

Richard Young told the seminar about his experiences of the last recession, and reflected on how one of our companies, Blue Prism, is adapting to the new reality in Enterprise Software by adapting their customer messaging and propositions.![]() They are conserving cash and looking to exploit their fast ROI as a differentiation in a cost-orientated market.

I liked Richard's comments that in the last recession, "it was noticeable that you knew when it was over because it was when people stopped talking about when it would end"!

My turn next, and I covered the stuff in my last post about how to think about the scale and rapidity with which early-stage companies should be reacting. If you have a look at that post there's a calculator where you can work out just how vulnerable your company might be.

We finished off with a lively debate on the impact and reactions that tech companies will feel over the next year.

They are conserving cash and looking to exploit their fast ROI as a differentiation in a cost-orientated market.

I liked Richard's comments that in the last recession, "it was noticeable that you knew when it was over because it was when people stopped talking about when it would end"!

My turn next, and I covered the stuff in my last post about how to think about the scale and rapidity with which early-stage companies should be reacting. If you have a look at that post there's a calculator where you can work out just how vulnerable your company might be.

We finished off with a lively debate on the impact and reactions that tech companies will feel over the next year.

Saturday, 4 October 2008

Silicon Valley Goes Dry? effects of the credit crunch on VC funding

Redherring trumpets that "Silicon Valley Goes Dry", in yet another report trying to figure out the impact of the current financial malaise on technology VC.

So far, I've come across all sorts of tales of doom, and in the RedHerring report the lack of M&A exits and IPOs (in part due to the lack of bank leverage) is cited as hitting exits- which in the next few months must be inevitable. It then goes on to suggest that "...the collapse of IPO and M&A markets mean they [VC funds] won’t be repaid as quickly. That means VCs won’t have funding to finance new companies or to add follow-on rounds for current companies". Erm, not exactly. Whilst lack of exits may hit some fund returns, if their timing is unfortunate particularly, VCs are normally not allowed to re-invest the returns from their exits. That means that VCs who have raised funds should still have the committed monies to invest from for some time. However, the other side of this coin is that VC funds do usually rely on their investors providing the cash in drawdowns to the funds as required. Normally as the fund's investors are financially solid, and once committed they are contractually obliged to follow-through, there is no financial risk to the fund itself. However, if any of the fund's backers fall, then that backer would be unable to meet its obligations. Should that happen then the fund's constitution often allows the other investors to choose to hang-on to their cash. That MAY mean that a small proportion of financial institutions falling, could cause some funds to "shut up shop" entirely. It's too early to say if this will happen much, but Venture beat certainly cast some doubt on at least one fund.

Fortunately, none of our backers appears in any way effected, but it does show how hard it will be for any of us to anticipate exactly how this crisis will play through to technology businesses.

Perhaps venture-backed businesses should start asking some questions of their VCs!

Thanks to Anders.B for the image.

Redherring trumpets that "Silicon Valley Goes Dry", in yet another report trying to figure out the impact of the current financial malaise on technology VC.

So far, I've come across all sorts of tales of doom, and in the RedHerring report the lack of M&A exits and IPOs (in part due to the lack of bank leverage) is cited as hitting exits- which in the next few months must be inevitable. It then goes on to suggest that "...the collapse of IPO and M&A markets mean they [VC funds] won’t be repaid as quickly. That means VCs won’t have funding to finance new companies or to add follow-on rounds for current companies". Erm, not exactly. Whilst lack of exits may hit some fund returns, if their timing is unfortunate particularly, VCs are normally not allowed to re-invest the returns from their exits. That means that VCs who have raised funds should still have the committed monies to invest from for some time. However, the other side of this coin is that VC funds do usually rely on their investors providing the cash in drawdowns to the funds as required. Normally as the fund's investors are financially solid, and once committed they are contractually obliged to follow-through, there is no financial risk to the fund itself. However, if any of the fund's backers fall, then that backer would be unable to meet its obligations. Should that happen then the fund's constitution often allows the other investors to choose to hang-on to their cash. That MAY mean that a small proportion of financial institutions falling, could cause some funds to "shut up shop" entirely. It's too early to say if this will happen much, but Venture beat certainly cast some doubt on at least one fund.

Fortunately, none of our backers appears in any way effected, but it does show how hard it will be for any of us to anticipate exactly how this crisis will play through to technology businesses.

Perhaps venture-backed businesses should start asking some questions of their VCs!

Thanks to Anders.B for the image.

Friday, 3 October 2008

Survey on Corporate Finance Advice

I was curious to see what the aggregated view of the portfolio companies was on Corporate Finance advice. So I asked our portfolio companies to give us some feedback which I've summarised below. Any comments would be very welcome!

Monday, 22 September 2008

Choosing an Entry Market Sector

A common issue I see with early-stage companies is over their selection of entry market sector. Obviously, all investors love their portfolio companies to have a huge vision to change large markets in a big way, and on occasion the best way to plan to reach that is to go straight to the big opportunity head-on. However, often that's going to be slow and hard, perhaps credibility is crucial, in which case it's really helpful to find a launch "beach-head" in the lines advocated by "Crossing The Chasm".

So where companies have chosen to use a beach-head, the next question is which one? If you just pick the "largest sector", or the one you're "most familiar with, you face a danger- the best entry sector is not always the obvious one. I think there's a different set of thinking about launch markets, where you highlight a slightly different set of factors as important.

| Criterion | Ultimate market | Launch market |

| Scale | Ideally as large as possible | Manageable, but low priority in selection process |

| Differentiation of offering against competition | Important | Critical |

| Focus on customer problems | Can be more general- boxed product is easier to scale | May be helpful to have solution type sales initially |

| Unit sale | Very large or small is good- scalability is crucial | Ideally ~1 months burn- large enough to be useful, but small enough to avoid lengthy approvals |

| Mission criticality | Mission critical to the customer provides extra value | Ideally not too critical- hard to buy from a startup |

| Length of buy cycle | May be long | Short is incredibly helpful |

| Easy customer identification | Useful | Vital |

I bet there are some great suggestions for improvements to this table- please let me know!

Wednesday, 10 September 2008

Plan B for Fundraising

Guy Kawasaki has an interesting post comparing the merits of bootstrapping vs. early VC backing which is well worth reading. He nicely positions bootstrapping as a Plan B, and certainly makes it appear quite an attractive option. My own take would be:

| Outcome | ||

| Product Sells | Product Doesn't Sell | |

| Venture Backed | You exit and have to share some of the rewards* with the VCs | The company fails and everyone is unhappy. |

| Bootstrapped | You exit, but probably only after raising some money to give yourself strategic options and thereby boost the price. | The company fails and everyone is unhappy. |

Friday, 5 September 2008

Technology Recruitment in an Early Startup

Daniel Tenner has a great post that is good reading for people looking to build early tech startups. I would just caveat his comments by suggesting that care is needed in understanding how you provide equity to those who help you out in those early steps. Daniel is completely right to suggest:

| "You want them to feel that it’s their company, and to do that, you have to give them equity - not options, not promises of options, but actual founder’s equity. Don’t feel like you’re giving stuff away here. If you’ve got the right person for the job, ensuring that they feel ownership of the company will ensure that your share is worth something. It’s better to own 70 or 80 or even 51% of something than 100% of nothing." |

- Ideal hires- people who you would've hired to do the job at the full commercial rate if only you had the cash, and who you'd expect to continue to be perfect for the job in 3-12 months time.

- Opportunistic hires- people who are prepared to get involved early, before an ideal candidate would join, but who are probably not long-term management or key staff.

Friday, 4 April 2008

Tuesday, 18 March 2008

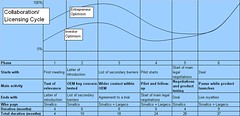

The Collaboration Cycle

Three months into licensing or pursuing a market entry for a new technology everyone involved always feels like they're a few months away from a deal, and no more than a year from revenue. Time and time again we've found it always takes much longer. You can expect to see at least one change in the bigco's team, and if it's an international collaboration each cycle of meetings takes months. This graph tries to compile the wisdom from all our companies licensing and collaboration projects- the conclusion being that, even without any hiccups, it's likely to take around 3 years from first meeting to revenue. This is a real opportunity, in my view, for the largeco's to steal a march on their competitors- getting really quick and sharp about technology acquisition would buy them a great advantage.

Monday, 17 March 2008

Rahns law of investment propositions

Mark Rahn, the newest member of our technology team, is doing a great job and took to the job like a "duck to water". He came up with a real gem of an observation the other day, which I've taken the liberty of christening, "Rahn's Law".

Mark Rahn, the newest member of our technology team, is doing a great job and took to the job like a "duck to water". He came up with a real gem of an observation the other day, which I've taken the liberty of christening, "Rahn's Law".

| "The quality of a proposition is inversely proportional to the amount of time the plan or team spends extoling its virtues." |

This links nicely to four tests for any business plan which I've always urged our investees employ:

Four tests for business plans

1. The superlative test

Have you obliterated all superlatives? Leave it to the judgement of the reader if something is really "exciting","superb", let alone is someone's track record is one of "success".2. Have you used facts/numbers wherever you can?

It's a good discipline to try and replace each superlative with a number or fact instead: it makes writing much punchier! Don't say there's a "multi-billion dollar market for mobile software", try and say something like "there's a £n million market for GPS software on mobile devices". It's a great deal harder to write this stuff, but it helps convey real market knowledge and understanding.3. Check that jargon is appropriate/necessary

If I was writing a plan associated with "WiMax", the I probably need to refer to "WiMax"; that's appropriate use of jargon. However, it doesn would a proposition really benefit from using "ARPU" when you're not talking about anything that's not encapsulated by the word "revenue".4. Can a non-specialist reader tell what the company provides?

Include a laymans explanation of what your product or service is/does. A good case-in-point is a company I've been reading about tonight: they provided three documents in total describing the business, but after reading them, I have only the vaguest idea what the business does. Without this information all the stuff about the team, route to market and competitors is really hard to understand, relate or assess.I'm sure there are some other great suggestions out there...?

Later ammendment

5. Did you really describe your competitors and their comparative attributes?

This is often one of the most revealing sections of a plan- it's amazing how often it's missing!Monday, 10 March 2008

Updated: Role of Chairman in Pre-Revenue Tech companies

The role of the chairman in RisingStars companies is a little different from the standard in a small company due to the emphasis on growth and support of a growing team.

Updated version, also I've added the highlights to emphasise particular areas that are unusually important in a pre-revenue technology company.

| Team Building |

|

| Financial Governance |

|

| Strategy |

|

| Fundraising |

|

| Representing Shareholders Interests |

|

| Proceedings at Board Meetings |

|

Tuesday, 4 March 2008

Top 30 Internet Start-ups- erm not!

Top 30 Internet Start-ups

Real Business published on "Thursday, 30th August 2007"

I stumbled across this fascinating article today.

The top 30 includes Beenz.com and Boo.com- so somehow I think that their content management system isn't getting the date of the article quite correct. Anyone care to guess the correct date?

Seriously, it makes interesting reading if you want to compare the original .com bubble to the web2.0 situation today. I don't think you'd be left with the impression that there was too much in common?

A more interesting comparison for me was in the IT suite of my kids (primary) school, the end wall had been peppered with around 25 Web2.0 services that they were suggesting the children might like to use for entertainment or for coursework. Interestingly very few of these were actually targeting children, no doubt many are putting out a free product with a view to building paying customers later. The most sobering thing was how few of these services I'd actually come across!

Friday, 8 February 2008

Government Agency does better Due Diligence than Investors- apparently!

So the "technical due diligence done by EEDA (East of England Development Agency) often exceeds that of investors"! According to the article on the Cambridge Network website this is because "EEDA pay for the Patent Office to carry out a patent search, and also send applications to at least two experts in organisations such as the National Physics Laboratory and National Engineering Laboratory".

So the "technical due diligence done by EEDA (East of England Development Agency) often exceeds that of investors"! According to the article on the Cambridge Network website this is because "EEDA pay for the Patent Office to carry out a patent search, and also send applications to at least two experts in organisations such as the National Physics Laboratory and National Engineering Laboratory".

I'm not sure if I'm more gobsmacked that the Development Agency that investors in their region do less DD than that, or that they put so much faith in the kind of reports they get from people like NPL and NEL to confirm the commercial potential of the innovations they see.

Thursday, 17 January 2008

Startup 2.0

Manoj threw another great event tonight with interesting speakers and audience alike. Stuart Scott-Goldstone of Aaron and Partners gave a thorough introduction to the range of legal issues that startups face on raising their first round of venture capital. the long list or issues seemed seems like it must be scary to any startup listening! Doug Stellman of YFM Private Equity started his presentation with a disclaimer of small print lest any of us fancied investing. Interestingly the proportion of Software and IT deals had shrunk from around 35% in 2006 to 20% in 2007, apparently due to concerns about the ease with which software companies could be established. His presentation focused on the management team as a key driver for their investment decisions. He cited that he sees applicants with a management team with a prior record of success "more often than you'd think". Paul Barraclough of TecMentor praised the Crossing the Chasm approach to getting to early sales momentum in startups. For me, Pam Holland gave the star presentation- starting off with a video (link to follow if I can persuade Pam to let me upload it) portraying how rapidly Telecity had grown pre-dotcom crash. She explained how they'd managed the spectacular growth in staff numbers and the attendant HR issues. I loved the story about how she had to persuade the founder to go home for his meal in the evening to encourage the staff to go home at night- even if he returned later each night! She explained the "competency based" recruitment approach she used, biased towards the attitude and raw capabilities of the individual rather than solely their technical skill-set. She also related that it was a "little bit disappointing" when the share price slumped from £23.00 to 2.3p, and she had to handle a new set of challenges!

Monday, 14 January 2008

So...Facebook is evil. Adverts are evil. Investors to be next?

Tom Hodgkinson at the Guardian has just published a bizzare piece about Facebook. Others better qualified will, I'm confident, tear it to pieces on a line-by-line basis, but I do get a little nervous that this view of the world it portrays. I recently met a very bright and capable young technologist, who'd done great work for charities on fundraising using some really creative techniques. Whilst he expressed interest in doing his own technology start-up one day, he came to the table with such a slanted view that "advertising was fundementally evil", that it makes me worry that Mr Hodgkinson represents a significant part of the population.

Facebook is dammed in this piece by loose association (via a shared investor and a specialist fund) with the CIA- and thus makes the implication that Facebook is really a CIA vehicle. Is this level of paranoia really so far from being clinically recognisable?

Tom Hodgkinson at the Guardian has just published a bizzare piece about Facebook. Others better qualified will, I'm confident, tear it to pieces on a line-by-line basis, but I do get a little nervous that this view of the world it portrays. I recently met a very bright and capable young technologist, who'd done great work for charities on fundraising using some really creative techniques. Whilst he expressed interest in doing his own technology start-up one day, he came to the table with such a slanted view that "advertising was fundementally evil", that it makes me worry that Mr Hodgkinson represents a significant part of the population.

Facebook is dammed in this piece by loose association (via a shared investor and a specialist fund) with the CIA- and thus makes the implication that Facebook is really a CIA vehicle. Is this level of paranoia really so far from being clinically recognisable?

Subscribe to: